Classification

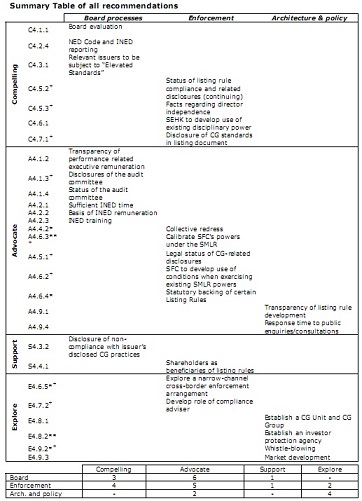

A total of 28 recommendations have been made. Twenty-two propose changes that can be made by regulatory agencies, two require a change to legislation, and another four may require legislative change subject to the outcome of a further consultative process.

Ten recommendations propose improvements to board processes that will foster transparency and accountability, including in relation to the role of the audit committee and independent directors.

Twelve recommendations address the ability of shareholders and regulators to conduct meaningful, and graded, enforcement where an issuer's practices fall below required CG standards.

Nine recommendations assist with ex ante enforcement concerns against non-Hong Kong incorporated companies.

Six recommendations address regulatory architecture and policy development that would work to better serve the interests of shareholders and the market.

Recommendations in this Report vary according to: whether or not they involve a change in legislation or may subsequently require such a change; the strength of evidence that supports it; and whether it is likely to be contentious to the industry.

Based on these variables, each recommendation has been assigned one of the following classifications:

Compelling (C) - Advocate (A) - Support (S) - Explore (E).

These are not «levels» per se, meaning that each may be worth developing or implementing for different reasons. Twenty recommendations fall into the «C» and «A» classification, with two and six falling into the «S» and «E» classifications, respectively.

Each recommendation is also denoted as follows:

* legislative change might be required depending on a subsequent enquiry;

** legislative change required;

+ assists in relation to non-Hong Kong incorporated issuers.

The recommendations made by this Report are summarized in the following sections. The references at the right side of each topic identify the recommendation number together with its classification as per above. A summary of all recommendations is provided in the Table at the end of this section.

Section 4 of the Report provides the detail of each recommendation together with a cross reference to the supporting analysis in Section 3 of the Report.?

Recommendations that do not require any change to the law

The changes can be made by the HKEX and the SFC working together or by the SFC alone.

The board

Hong Kong's CG standards imposed by non-statutory regulations on the board are broadly in line with international best practices. However, board directors remain insufficiently accountable to shareholders in terms of performance evaluation and executive remuneration. The audit committee's ability to reach its full potential is handicapped because of the limited delegated power they are typically provided by the board. The expected role of non-executive directors (NEDs) that are not independent is not always clear. While the requirement for independent non-executive directors (INEDs) has been introduced as a check on executive power, the existing framework does not sufficiently support and foster the functionality of the intended role.

Recommendations that improve the transparency and accountability of the board:

|

Topic |

Proposed |

Ref. |

|

Board evaluation |

Require the board, on a comply or explain basis, to undertake an annual self-evaluation based on a disclosed evaluation policy that covers specified matters including high-level terms of reference and the involvement of INEDs or external advisers. The board to report annually on how it has complied with the provision and specified matters including, for example, how the evaluation was undertaken and whether any recommendations are made. This builds on developments in the UK, Mainland China and Singapore. |

C4.1.1 |

|

|

Step required: Amend CG Code (Appendix 14 listing rules). |

|

|

Executive remuneration |

Require disclosure of the considerations taken into account by the remuneration committee in relation to any performance- linked remuneration. This builds on developments in the UK and the United States. |

A4.1.2 |

|

|

Step required: Amend the listing rules & CG Code (Appendix 14 listing rules). |

|

|

Audit committee |

Require the audit committee to itself make a disclosure in the annual report including as to its role in relation to the external audit process and the work it has undertaken to discharge its responsibilities. The independence and accountability of the audit committee can be improved through increased visibility. This builds on developments in the UK and the United States. Require the board, on a comply or explain basis, to delegate all A4.1.4 powers in relation to the appointment, compensation, and oversight of the external auditor to the audit committee. This builds on developments in the United States. |

A4.1.3+

A4.1.4 |

|

|

Step required: Amend the listing rules & CG Code (Appendix 14 listing rules). |

|

|

Non-executive & independent directors |

Require issuers to develop and disclose, on a comply or explain basis, a code for NEDs (NED Code) that specifies its policies, practices and expectations in respect of INEDs and other NEDs that is designed to facilitate the effectiveness of NED roles. The CG Code to provide a Model NED Code that an issuer may choose to comply with or alternatively establish their own NED Code via policies that address the NED's expected involvement, sufficiency of a NED's time, basis of remuneration, and knowledge of the business and training, etc. The Code based approach provides a clearer forum for establishing the expectations placed on INEDs and other NEDs. In addition, INEDs are to be required to report annually on their activities and the effectiveness of the NED Code. This builds on requirements in the United States, Mainland China, Singapore and the UK. |

A4.2.1 A4.2.2 A4.2.3 C4.2.4

|

|

|

Step required: Amend CG Code (Appendix 14 listing rules). |

|

Enforcement

The extent to which the enforcement regime in Hong Kong has fallen behind international practices is significant. Shareholders in issuers listed in Hong Kong are in various ways worse off when compared to their counterparts in other major markets.

It is widely recognized that disclosures made under the listing rules form part of the total mix of information used for exercising voting rights and making investment decisions. Shareholders have a reasonable expectation that issuers should comply with the listing rules. Despite the foregoing, shareholders have no rights where the company and its directors have breached the listing rules, unless it also amounts to a breach of law.

The position of shareholders is made worse by the absence of a world-class regulator¬based enforcement regime, a shortcoming that arises out of a significant enforcement lacuna between the disciplinary sanctions imposed by The Stock Exchange of Hong Kong Limited (SEHK) and the powers available to the SFC. This enforcement lacuna is not a product of regulatory architecture per se. Regulatory agencies can make better use of extant powers or bring other administrative powers to bear on CG sensitive topics. For example, section 384(3) of the SFO is a provision designed by the legislature to be by regulatory agencies to safeguard the performance of their statutory functions being supplied with false or misleading information, but the section has not extensively utilised.

While much has been written on the HKEX's potential conflict of interest, there is little discussion on the other considerations the SFC must take into account when deciding whether to bring an action that would benefit shareholders.

Recommendations that improve the ability of shareholders to seek redress against wrongdoing issuers and directors:

|

Topic |

Proposed |

Ref. |

|

Listing rules |

Give shareholders rights to enforce any disclosure breach of the listing rules by making them third party beneficiaries of the contract between the issuer and the SEHK. This builds on experiences in the United States and the ability of shareholders in the UK and Singapore to bring actions. |

S4.4.1 |

|

|

Step required: Amend the listing rules. |

|

|

Recommendations that improve the transparency and accountability of an issuer's CG- related disclosures and assist to close out the SEHK-SFC enforcement lacuna:

|

||

|

Topic |

Proposed |

Ref. |

|

Listing rule disclosures |

Four types of CG-related disclosures to be required to be made on a form that brings the disclosure within section 384(3) of the SFO under which providing false or misleading information to a regulator is an offence: (1) existing required disclosures concerning financial disclosure, notifiable and connected transactions, and those made pursuant to the CG Code; (2) breaches of the listing rules are to be disclosed on an ongoing basis; (3) an annual certification of compliance with the listing rules will be required; and (4) facts pertaining to independence disclosed to the SEHK by a proposed INED. This reflects standards already in place in the United States, the UK, Singapore and Mainland China. |

A4.5.1+ C4.5.2+ C4.5.3+ |

|

|

Step required: Amend listing rules and CG Code (Appendix 14 listing rules). |

|

|

SEHK discipline |

The SEHK to make more effective use of its existing powers (1) to require issuers to “take, or refrain from taking, such other action as it thinks fit” and (2) to impose resumption conditions on suspended issuers. In both cases, issuers and/or directors can be required to take steps that address specific CG shortcomings. |

C4.6.1 |

|

|

Step required: Better utilization of an existing power. |

|

|

SMLR conditions |

The SFC to use its power to impose conditions on listing applicants or issuers that would work to address the underlying CG shortcomings or failures that gave rise to the problem, and that may serve to catalyze change. |

A4.6.2+ |

|

|

Step required: Better utilization of an existing power. |

|

|

Recommendations that improve CG standards from the outset of an issuer's listing on an ex ante basis (gate keeping):

|

||

|

Topic |

Proposed |

Ref. |

|

Listing applicant standards |

Require a listing applicant to make a statement in the listing document cum prospectus explaining its current CG practices and how these will be developed in the period to its next annual report in view of the standards imposed and expected under the listing rules and the CG Code. Require the sponsor's declaration to encompass the foregoing. This builds on the requirements in the United States. |

C4.7.1+ |

|

|

Step required: Amend the listing rules. |

|

|

Compliance adviser |

Upgrade the compliance adviser role to make it more active,engaged and responsible. A sponsor to the listing application should undertake the role. Prior to termination, a declaration to be made by the compliance adviser as to the completion of its role on a form subject to section 384(3) of the SFO. This builds on the requirements in Mainland China. |

E4.7.2+ |

|

|

Step required: Amend the listing rules. |

|

CG standards generally

Apart from standard setting and enforcement, good CG standards require promotion, as do departures from them. The largest issuers in the UK are subject to higher standards, and this forms a positive association between expectations of good CG and successful companies. Many issuers on the Hang Seng Index already adhere to higher standards and this should receive more visible endorsement.

Recommendations that promote CG standards generally:

|

Topic |

Proposed |

Ref. |

|

Elevated standards |

Impose higher standards on designated issuers such as HSI or HSCEI constituent stocks. Selected recommended best practices become comply or explain provisions, and selected recommended disclosures become required disclosures for those issuers as “Elevated Standards”. Consideration to be given to incorporating specified comply or explain provisions as mandatory requirements in the Elevated Standards. This builds on experiences in the UK. |

C4.3.1 |

|

|

Step required: Amend CG Code (Appendix 14 listing rules) and/or listing rules. |

|

|

Departure from adopted practices |

Issuers may adopt CG practices that are not mandated by the listing rules and although variations from those practices may not amount to a breach of the listing rules, they are nevertheless relevant to an investors' legitimate interest in the CG practices of an issuer. Accordingly, the changes should be disclosed if not merely temporary. (Note this is distinct from recommendations A4.5.1+ and C4.5.2+.) |

S4.3.2 |

|

|

Step required: Amend the listing rules. |

|

Policy development

Hong Kong needs to do better when compared with its international peers as regards developing CG policy that takes into account shareholder interests. Hong Kong lacks an unconflicted agency that is charged with this responsibility. Transparency of listing rule development as regards the matters considered by the SEHK and SFC is also lacking, and this is something likely to become of greater importance as courts or tribunals may be increasingly faced with the challenge of interpreting listing rules.

|

Topic |

Proposed |

Ref. |

|

CG Unit & CG Group |

Establish a CG Unit within a regulatory agency charged with CG policy development. It should be advised by an external market-based CG Group. If the proposal to establish an investor protection agency is adopted (see E4.8.2** below), it should be located within that agency. This is based on developments in the United States, and experiences in Hong Kong in relation to other regulatory concerns. |

E4.8.1 |

|

|

Step required: Identify agency to establish. |

|

|

Listing rule development |

The SEHK and SFC should provide ex post transparency to the explanations of purpose and likely effect required by the SFO to support listing rule development. |

A4.9.1 |

|

|

Step required: Adoption of relevant policy on transparency. |

|

|

Market development |

Undertake a clearer and more specific examination of what overarching objectives should drive the development of the Hong Kong market and the alternative mechanisms for shareholder protection that may need to develop in tandem with change, which may or may not require modification of the one-share-one-vote principle. |

E4.9.3 |

|

|

Step required: Undertake policy-led initiative. |

|

|

Agency response time |

Regulatory and government agencies undertaking consultations should voluntarily adopt a performance standard on response times. |

A4.9.4 |

|

|

Step required: Adoption of relevant policy on performance. |

|

Recommendations that require a change in the law

The changes can only be made by or with the approval of the Legislative Council, and so require sufficient political support from that body.

As noted above, the major shortcoming of Hong Kong's CG system is the enforcement lacuna. While the dual responsibilities model gives rise to some problems as discussed in this Report, they are not exclusive to that model. Rule making and rule-enforcement are separate matters that can be developed differently while also keeping within the dual responsibilities model. Given the SFC's ultimate powers under the model, its enforcement powers can be developed within the scope of the model. Other mechanisms of enforcement can also be developed outside the model, and this would include some of the enforcement developments suggested above that do not require any change to legislation.

|

Topic |

Proposed |

Ref. |

|

SMLR powers |

Calibrate SFC's powers to provide for a fine together with the imposition of conditions that works as a warning-cumprecursor to suspension that is premised on the same grounds as its existing SMLR powers. This can work as a win-win-win for the issuer, its shareholders and the market. The power is exercisable by the SFC directly as a specified decision subject to appeal to the Securities and Futures Appeals Tribunal, subject to prior consultation with the Listing Committee. This reflects powers already given to regulators in the UK, Singapore, Mainland China and, in certain regards, the United States. |

A4.6.3**+ |

|

|

Step required: Amend SMLR. |

|

|

Investor protection agency |

Establish a new, unconflicted regulatory agency empowered to bring an action for the benefit of shareholders. This is based on developments in the United States. |

E4.8.2** |

|

|

Step required: Amend the SFO or create new primary legislation. |

|

Recommendations subject to further enquiry

These are recommendations where any change is contingent on a further consultation or enquiry collecting more detailed evidence. Depending on the outcome, it may require changes that can only be made by the Legislative Council.

There remain a few significant issues Hong Kong's CG system must resolve but which cannot be described as a deficiency since experiences both internationally and locally remain mixed. First, the question of whether all or part of the listing rules should be given statutory backing remains under discussion but there has been little detailed exploration of the issue since 2013 when Hong Kong took a partial step in this direction with the implementation of Part XIVA of the SFO. Second, while the rights of shareholders under the law in relation to director misfeasance and mis-disclosure match or better international best practices, the difficulty of shareholders to act upon those rights is evidenced by the absence of legal actions that are taken and suggests more needs to be done to meaningfully give effect to shareholders' legal rights. Third, Hong Kong's piecemeal approach to whistle-blowing has clearly fallen behind international practices that give legal protections to whistle-blowers, and so represents the absence of a mechanism that might promote the discovery of wrongdoing. Each of these involve significant and far reaching issues on which more evidence would need to be collected for further evaluation.

Recommendations that require further detailed study:

|

Topic |

Proposed |

Ref. |

|

Statutory backing to listing rules |

Re-examine, in view of today's circumstances, the discussion on giving statutory backing to specific provisions of the listing rules - Chapters 4 (periodic financial reporting), 14 (notifiable transactions) and 14A (connected transactions). Undertake a detailed assessment of past problems under these Chapters of the listing rules. This reflects developments in the UK and Singapore. |

A4.6.4* |

|

|

Step required: Undertake a public enquiry/consultation. |

|

|

Cross-border enforcement |

To consider the feasibility of expanding the existing cross- border enforcement arrangements to create an arrangement with Mainland China specifically tailored to the public capital market within an agreed scope of non-criminal disclosure obligations. |

E4.6.5*+ |

|

|

Step required: HKSAR Government to consider exploring the issue with the Government of China. |

|

|

Statutory rights |

Re-visit, and develop, the Law Commission's 2012 proposal on the implementation of class action rights to widen its approach to collective redress. This builds on a process previously commenced in Hong Kong without conclusion, developments in the UK and Mainland China, and the position in the United States. |

A4.4.2* |

|

|

Step required: Undertake a public enquiry/consultation. |

|

|

Whistleblowing |

Commence an enquiry on whether to implement whistle-blowing laws, and whether this should be limited to specific circumstances such as corporate misfeasance. This builds on experiences in the UK, United States and Mainland China. |

E4.9.2*+ |

|

|

Step required: Undertake a public enquiry/consultation. |

|